How your rates bill is calculated

Each year Council determines how much it needs to raise from rates and charges to fund and improve our Shire’s facilities and services.

Council then divides this required revenue by the total Capital Improved Value (CIV) of all rateable properties to create a rate in the dollar. (This rate cannot exceed the rate cap created by Victoria’s Essential Services Commission.) This rate is then applied to the Capital Improved Value of your property to determine your general rates.

Different rates are applied to different property types. This is called differential rating.

Waste management (fixed) charges, plus the Victorian Government’s Fire Services Levy, are added to create your total rates bill.

Watch this video for further clarification on how your rates are calculated and how rate capping works.

Waste and other charges

In addition to your general rates, other charges may also be included in your rates bill.

In 2024/2025 they are:

Waste Management charge $230

This is levied on all properties to help fund the cost of maintaining waste disposal facilities in the Shire. It is not used to fund landfill/general waste collection and disposal.

Kerbside landfill/general rubbish – TOWNSHIP- collection $120 (Red-lidded bin)

This covers the cost of collecting and disposing of household rubbish from all dwellings within the township defined rubbish collection areas in our Shire. The charge is compulsory for dwellings whether the service is used or not. The service uses a 120-litre wheelie bin collected fortnightly.

Kerbside landfill/general rubbish – RURAL - collection $140 (Red-lidded bin)

This charge covers the cost of collecting and disposing of household rubbish from all dwellings within defined collections areas. This charge is compulsory for dwellings who have not opted out of the fortnightly collection service when it was introduced. A 140-litre wheelie bin is collected fortnightly.

Kerbside mixed recycling collection $110 (Yellow-lidded bin)

This charge covers the cost of collecting and processing mixed recycling in a 240-litre wheelie bin, provided by Council, fortnightly. This service is for township, rural and commercial properties. Commercial properties can elect to have this service to make their own arrangements for it to be collected privately.

Kerbside food and garden organics collection $190 NEW SERVICE IN 2024-2025 (Lime green-lidded bin)

This charge covers the cost of collecting and processing (locally in Creswick) organic material in a 120-litre wheelie bin, provided by Council, weekly. This service is for township properties. The service is also provided to those commercial properties (within township boundaries) who elect to have this service.

Kerbside landfill/general rubbish – COMMERCIAL- collection $485 (Red-lidded bin)

Council general rubbish service to commercial properties is optional. Operators of these properties can choose to make their own arrangements to have their rubbish collected privately. However, where the Council service is used a 240-litre wheelie bin is provided for weekly collection. For more information on our commercial services visit commercial waste.

Property Based Fire Services Levy-Fixed and Variable

This is the Victorian Government's property-based levy to fund firefighting services in Victoria. All property owners pay the levy at the same time as they pay council rates. Council collects the levy through rate notices on behalf of the State Government. The levy is calculated based on the capital improved value of your property. It consists of a fixed component plus a variable component.

The Fixed Levy is $132 for residential properties and $267 for non-residential properties.

The Variable Levy will differ for property types such as residential, industrial, commercial and primary production. This portion of the levy is calculated as a percentage of CIV. Eligible pensioners are entitled to a $50 rebate against the Fire Services Levy for their principal place of residence.

Municipal and Environmental Charge

The fixed fee for both the Municipal Charge and the Environmental Charge has been abolished.

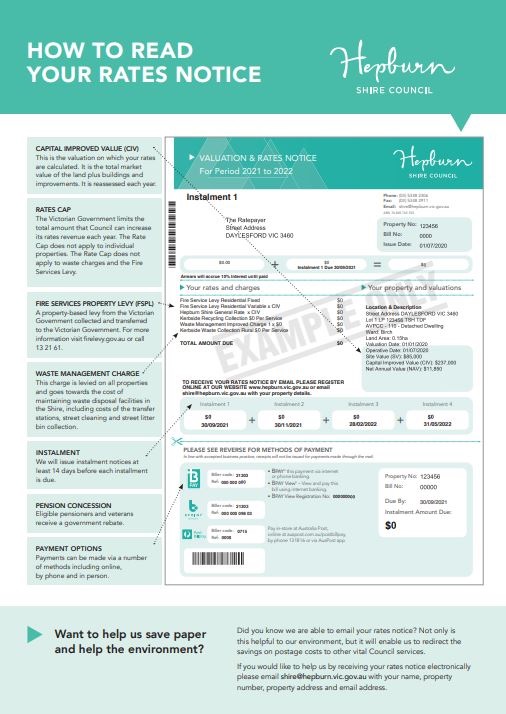

How to read your rates notice

(PDF, 289KB)

(PDF, 289KB)